Предположим, вы хотите, чтобы выборка была достаточной для некоторых процентилей, чтобы не переборщить. Вот код:

quantile.CI <- function(n, q, alpha=0.1) {

#

# Search over a small range of upper and lower order statistics for the

# closest coverage to 1-alpha (but not less than it, if possible).

#

u <- qbinom(1-alpha/2, n, q) + (-2:2) + 1

l <- qbinom(alpha/2, n, q) + (-2:2)

u[u > n] <- Inf

l[l < 0] <- -Inf

coverage <- outer(l, u, function(a,b) pbinom(b-1,n,q) - pbinom(a-1,n,q))

if (max(coverage) < 1-alpha) i <- which(coverage==max(coverage)) else

i <- which(coverage == min(coverage[coverage >= 1-alpha]))

i <- i[1]

#

# Return the order statistics and the actual coverage.

#

u <- rep(u, each=5)[i]

l <- rep(l, 5)[i]

return(list(Interval=c(l,u), Coverage=coverage[i]))

}

###bootstrap alternative method############

quantile.CI.via.bootstrap <- function(x, p, alpha = 0.1) {

## Purpose:

## Calculate a two-sided confidence interval with confidence level of (1 - alpha) for

## a quantile, based on the (computing intensive) bootstrap resampling method.

##

## Arguments:

## - x: a vector of values, representing a data sample.

## - p: probability cutpoint for the quantile (between 0 and 1).

## - alpha: type I error level (default to 0.1 so a 90% CI is calculated)

##

## Return:

## - CI: the lower and upper limits of the two-sided CI.

q <- quantile(x, probs = p)

message("Quantile Point Estimate = ", q, " (Probability Cutpoint = ", p, ")\n")

## Bootstrap resampling with 2000 replications

library(boot)

set.seed(1)

b <- boot(x, function(x, i) quantile(x[i], probs = p), R = 2000)

boot.ci(b, conf = 1 - alpha, type = c("norm", "basic", "perc", "bca"))

}Первый метод реализует метод Hahn & Meeker 1991, а второй является просто непараметрическим бутстрапом.

n.s<-seq(50,200,5)

q.90<-0.90 #less strict

q.99<-0.99

results.90<-matrix(NA,2,length(n.s))

results.99<-matrix(NA,2,length(n.s))

for (i in 1:length(n.s)){

lu.90 <- quantile.CI(n.s[i], q.90)$Interval

results.90[1,i]<-lu.90[1]

results.90[2,i]<-lu.90[2]

lu.99 <- quantile.CI(n.s[i], q.99)$Interval

results.99[1,i]<-lu.99[1]

results.99[2,i]<-lu.99[2]

}

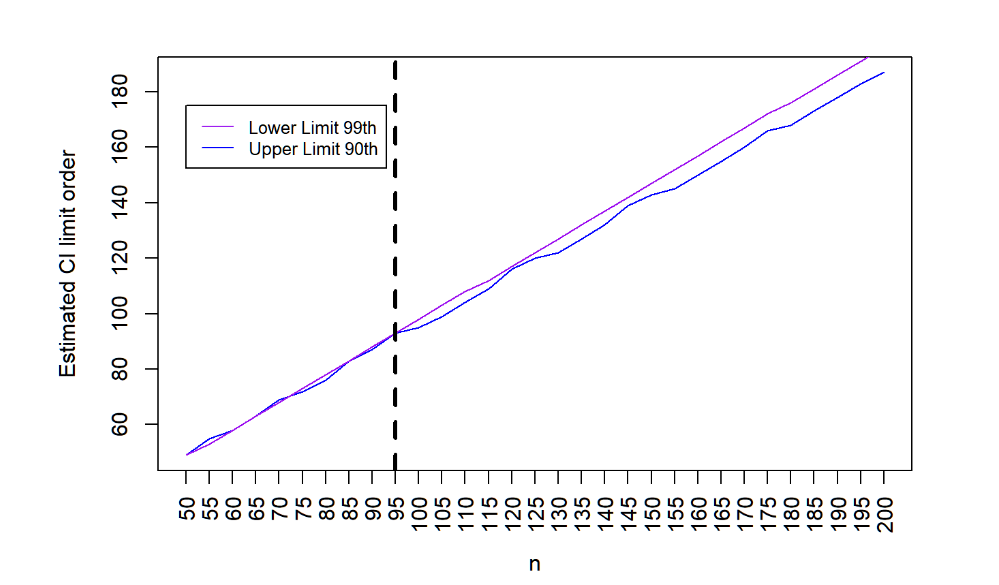

plot(results.90[2,],ylab="Оценочный CI лимитного ордера",xlab="n",type="l",col="blue",axes=FALSE,pch=19)

ось(2)

axis(1, at=seq_along(results.90[1,]),labels=as.character(n.s), las=2)

box()

lines(results.99[1,],col="purple",type="l",pch=18)

abline(v = which(n.s==95), col="black", lwd=3, lty=2)

# Добавьте легенду

legend(1, 175, legend=c("Нижняя граница 99-й", "Верхняя граница 90-й"),

col=c("purple", "blue"), lty=1, cex=0.8)

Как мы видим, выборка n=95 является достаточной согласно методу бутстрапа.

Результаты бутстрапа:

n.s<-seq(50,200,5)

q.95<-0.90

q.99<-0.99

results.95<-matrix(NA,2,length(n.s))

results.99<-matrix(NA,2,length(n.s))

for (i in 1:length(n.s)){

x <- rnorm(n.s[i], mean = which.mean.max, sd = which.sd.max) 1TP5Тут самый большой CV

lu.95 <-quantile.CI.via.bootstrap(x, 0.90, 0.1)$bca

results.95[1,i]<-lu.95[4]

results.95[2,i]<-lu.95[5]

lu.99 <- quantile.CI.via.bootstrap(x, 0.99, 0.1)$bca

results.99[1,i]<-lu.99[4]

results.99[2,i]<-lu.99[5]

}

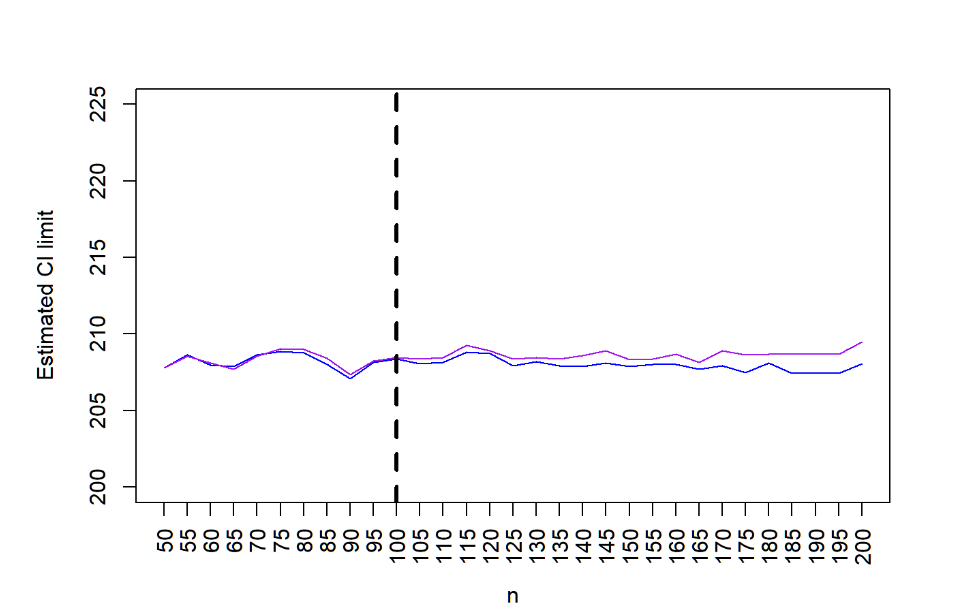

plot(results.95[2,],ylab="Предполагаемый предел CI",xlab="n",type="l",col="blue",axes=FALSE,pch=19,ylim=c(300,400))

ось(2)

axis(1, at=seq_along(results.95[1,]),labels=as.character(n.s), las=2)

box()

lines(results.99[1,],col="purple",type="l",pch=18)

abline(v = which(n.s==100), col="black", lwd=3, lty=2)

# Добавьте легенду

legend(1,5 , legend=c("Нижняя граница 99-й", "Верхняя граница 90-й"),

col=c("purple", "blue"), lty=1, cex=0.8)

Согласно результатам бустрепа, достаточно 100. Обратите внимание, что здесь используются оценки типа BCA в бутстрэп-выборках, которые являются робастной версией.

Не то чтобы оба метода были свободными от распределений, непараметрическими!

Вы можете использовать их и для других процентилей. Веселитесь!